European Job Market 2026: Data, Trends, and Projections for Business Leaders

The headline number is deceptively positive: EU-27 unemployment sits at approximately 5.9%, a historic low. But the European job market in 2026 is not a single story of labor market health. It is four simultaneous transformations playing out at different speeds across different economies, sectors, and demographics, with business strategy implications that require nuanced interpretation.

This analysis synthesizes current data from Eurostat, the ILO, McKinsey Global Institute, and the World Economic Forum to give business leaders and HR executives an accurate picture of where the European labor market stands, which structural forces are reshaping it, and what that means for workforce planning over the next three to five years.

What is the European Job Market?

The European job market collectively describes employment conditions, labor demand and supply dynamics, skills markets, and workforce regulatory frameworks across the 27 EU member states and their immediate neighbors. It is not a single market in the economic sense — each country maintains distinct labor law, wage-setting mechanisms, social protection systems, and workforce composition — but the free movement of workers across EU borders creates meaningful integration that makes pan-European analysis essential for organizations operating across member states.

In 2026, the European job market is defined by five intersecting structural forces: post-pandemic normalization, AI-driven task automation, the green energy transition, demographic aging, and an accelerating digital skills shortage. Each force operates simultaneously, creating a complex strategic environment for organizations managing talent across the continent.

The Numbers: Where the European Job Market Stands

Unemployment: Record Low, But Diverging

EU aggregate unemployment reached 5.9% by Q4 2024 (Eurostat), the lowest recorded rate since the measure's inception. The data by country tells a more complex story:

Country | Unemployment Rate (2024) | Youth Unemployment |

|---|---|---|

Germany | 3.4% | ~6% |

Netherlands | 3.7% | ~8% |

Poland | 2.8% | ~5% |

Czech Republic | 2.6% | ~5% |

France | 7.3% | ~17% |

Italy | 6.5% | ~21% |

Spain | 11.5% | ~25% |

Greece | 10.4% | ~23% |

EU-27 Average | 5.9% | ~14.5% |

The divergence between northern/eastern Europe (effectively at full employment) and southern Europe (elevated unemployment, severe youth unemployment) is one of the defining structural features of the European labor market and shows no sign of rapid convergence.

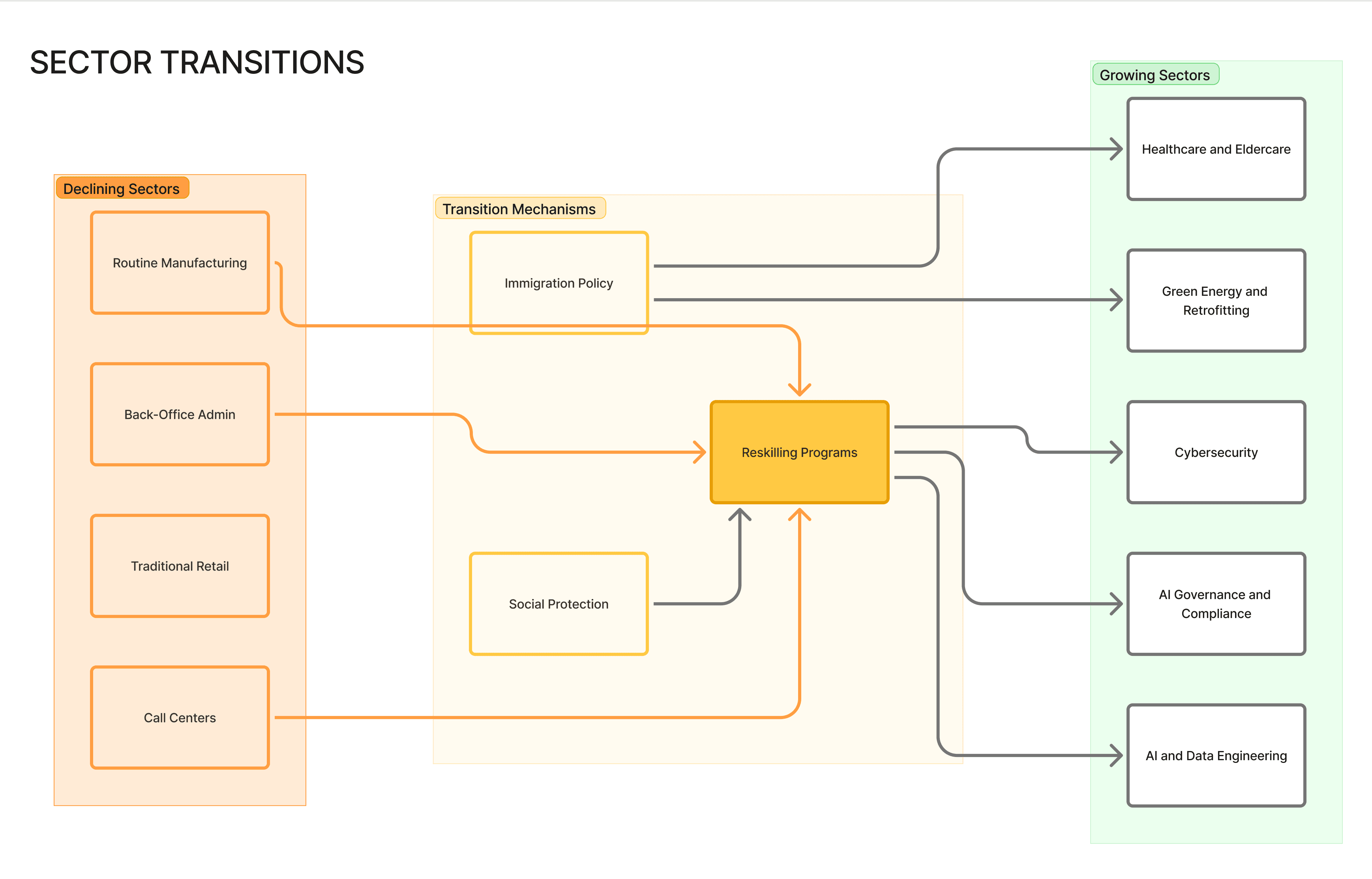

Sector Growth and Decline

Technology and digital services continue to add roles faster than any other sector, with particular strength in AI, cybersecurity, data science, and cloud infrastructure. Healthcare and eldercare are expanding due to demographic demand. Renewable energy and building retrofitting show consistent growth tied to green transition investment.

The sectors under pressure are equally clear: manufacturing roles involving routine tasks, administrative and back-office functions in financial services, call center and customer service operations at scale, and mid-skill data entry and processing roles across all industries.

The labor market transformation following diagram illustrates the key flows:

The Five Structural Forces Reshaping European Employment

1. AI-Driven Task Automation

McKinsey Global Institute estimates that by 2030, up to 30% of current work tasks in Europe could be automated: primarily in repetitive cognitive tasks (data processing, document review, routine correspondence) and standardized physical tasks (assembly, sorting, basic logistics). This is not job elimination; it is task reallocation.

Task automation does not equal job elimination at equivalent rates.

The sectors with highest task automation exposure:

- Financial services back-office: 40–55% of tasks susceptible to AI automation

- Public administration: 35–50% of tasks (document processing, data entry, standard inquiries)

- Retail and customer service: 30–45% (returns processing, standard queries, inventory management)

- Legal services: 25–40% (document review, contract analysis, research)

The critical distinction that organizational strategy must internalize: task automation does not equal job elimination at equivalent rates. A financial analyst whose compliance reporting is automated can cover more clients. A lawyer whose document review is automated handles more complex cases. The economic value remains; the skill requirements shift upward.

Sectors experiencing strong employment growth due to AI:

- AI and ML engineering (growing at 40%+ annually in EU postings)

- AI governance, ethics, and compliance (new category, high demand)

- Prompt engineering and AI operations

- Cybersecurity (AI-powered attacks increase demand for human defenders)

2. The Digital Skills Gap: Europe's Strategic Vulnerability

The European Commission's Digital Decade 2030 program sets a target of 80% of EU adults with basic digital skills. The current figure is approximately 54%. This 26-percentage-point gap represents one of Europe's most consequential economic vulnerabilities.

At the specialized end, the EU is estimated to face a shortage of approximately 4.2 million ICT professionals by 2027. This shortage is not evenly distributed. It is concentrated in AI-specific skills (ML engineering, data science, AI governance) and cybersecurity, where demand is growing at 25–40% per year while graduate supply grows at 5–8%.

Business implications are direct:

- Hiring timelines for digital roles are 40–60% longer than for equivalent non-digital roles in most EU markets

- Compensation premiums for AI skills are running 30–50% above base market rates for comparable seniority

- Companies are shifting toward skills-based hiring, internal development programs, and selective immigration to address the structural shortage

Gender dimension: women represent only 19% of the EU digital workforce. Beyond the equity imperative, this represents an enormous underutilized talent pool. Organizations that actively recruit and develop women for digital roles are accessing a less competitive talent segment.

3. The Green Transition: Net Positive with Concentrated Pain

The European Green Deal and REPowerEU investment programs are creating consistent demand for skilled workers in:

- Solar and wind installation and maintenance (growing at 20%+ annually)

- Building energy efficiency retrofitting (accelerating from 2025)

- Electric vehicle manufacturing and service (displacing conventional automotive roles)

- ESG reporting, climate risk assessment, and sustainability management

The European Commission estimates approximately 1.5 million net new jobs will be created by the green transition by 2030. However, the job creation and destruction are not geographically aligned. Coal mining regions (Silesia, Ruhr, parts of Czech Republic and Romania), conventional automotive clusters (Stuttgart, Wolfsburg), and carbon-intensive manufacturing areas face concentrated displacement that social protection systems are not yet adequately designed to address.

4. Demographic Pressure: The Structural Constraint Beneath Everything

Europe's labor market headline statistics operate against a backdrop that becomes more challenging each year: the working-age population is declining. EU citizens aged 20–64 are projected to decrease by approximately 3 million by 2030 as the large post-war generation cohort exits the workforce faster than younger cohorts replace it.

This demographic shift creates structural labor shortages that automation cannot fully resolve in the medium term—particularly in:

- Healthcare and eldercare (1.2 million additional workers needed across EU by 2030)

- Early childhood education (growing demand as participation rates increase)

- Essential services and trades (electricians, plumbers, care workers)

Germany's situation is the most acute: a projected shortage of 1.5 million skilled workers by 2030 that the country is addressing through expanded immigration pathways (the 2023 Skilled Worker Immigration Act), aggressive corporate upskilling programs, and AI adoption to extend existing worker productivity.

5. Post-Pandemic Normalization: Hybrid Work as Permanent Structure

Remote and hybrid working arrangements, adopted at scale during 2020–2022, have proven more durable than many expected. By 2025, approximately 38% of EU knowledge workers operate in hybrid arrangements (at least some remote work), and fully remote arrangements account for approximately 13%.

This structural shift has labor market implications beyond individual employee preference:

- Geographic labor markets for knowledge work have partially merged across EU member states. German companies routinely hire Polish engineers working remotely; Dutch firms access Portuguese digital talents.

- Office real estate demand in major cities remains below pre-pandemic levels, with second-tier cities gaining knowledge worker population.

- Compensation convergence: remote work has moderated some of the wage premium for living in high-cost capitals.

Build-versus-buy-versus-develop decisions made today about AI talent, for example, will determine competitive positioning for a decade.

What This Means for Business Leaders: Four Strategic Implications

Strategic Implication 1: Workforce Planning Must Extend to 2030

The labor market forces reshaping Europe are structural, not cyclical. Organizations planning workforce strategy on 12–18 month cycles are mis-calibrated for the environment. The structural shortage of digital and green skills, the growing demographic constraint, and the AI-driven task reallocation are all operating on 5–10 year timescales. Build-versus-buy-versus-develop decisions made today about AI talent, for example, will determine competitive positioning for a decade.

Strategic Implication 2: The Skills Transition is a Core Business Competency

The companies that navigate the labor market transformation successfully in Europe will be those that develop internal capability for skills identification, development, and redeployment; rather than relying primarily on external hiring into a structurally short talent market. Amazon's Career Choice program and SAP's skills initiatives are not charity; they are strategic responses to supply constraints that external hiring cannot resolve at acceptable cost.

Strategic Implication 3: AI Adoption and Workforce Transition Must Be Managed Concurrently

Organizations that adopt AI for task automation without explicit workforce transition planning face two risks: reputational damage from perceived job destruction (which affects employer brand and recruiting), and operational disruption from inadequate human capacity in the new AI-augmented roles. The companies executing this transition well (KPMG's AI-augmented audit teams, Deutsche Bank's AI-assisted operations) are managing AI deployment and workforce development as a single integrated program.

Strategic Implication 4: Location Strategy is a Talent Strategy Decision

The divergences in the European labor market make location meaningful. Setting up AI engineering operations in Lisbon or Warsaw offers access to large, growing, high-quality technical talent pools at significant compensation savings compared to London, Amsterdam, or Munich. The integration of European labor markets through remote work makes some of these trade-offs available without physical relocation. Organizations without an explicit European talent geography strategy are leaving both quality and cost advantages on the table.

Frequently Asked Questions

Conclusion

The European job market in 2026 presents a set of strategic paradoxes that require careful interpretation: historically low unemployment alongside structural skills shortages; strong employment growth in some sectors alongside acute displacement in others; a demographic workforce decline alongside the emergence of productivity-enhancing AI technology.

The organizations that will navigate this environment successfully are those that treat workforce strategy as a long-horizon, continuously updated discipline rather than an annual planning exercise. The data is clear on direction: digital skills will be increasingly scarce and valuable, green and care jobs will grow, AI will transform but not primarily eliminate most roles, and the demographic clock is working against simple reliance on external hiring.

The data is also clear on what this environment rewards: investment in people, clarity on skills needs, and strategic patience in building capabilities that external markets cannot supply at the pace and cost the business requires.

——

External Links

- Eurostat Employment Statistics - primary data source

- WEF Future of Jobs Report 2025 - sector projection data

- Further Reading